Here’s what the Simon-Kucher Global Telecom Study 2026 data says.

Telcos are currently losing commercial ground because customers are struggling to justify the value of the offerings in the market. Only 54% of consumers globally rate telco services as good value for money. That is a slight improvement (+4pp year on year), but it still leaves nearly half of customers questioning whether what they pay reflects what they receive. The gap is also uneven by region: MENA and Latin America show stronger value perception compared to more mature markets such as Europe and North America.

This matters because value perception is now showing up across the commercial system: declining ARPU, rising switching intent, weaker premium differentiation, and growing pressure from budget players and MVNOs.

Authors: Kajetan Zwirglmaier, Partner/Simon-Kucher; Alexander Zimm, Senior Director/Simon-Kucher

The premium edge is gone

This price-value mismatch directly impacts revenue. Since 2024, average monthly mobile spend has declined across all segments: premium at a CAGR of -2.6%, budget at -2.3%, and mid-market at -0.5%. The ones making headway are competing on brand, customer experience, and service quality, but premium monetization is becoming harder to defend.

One reason is feature parity. What once justified a premium price tag is increasingly available from budget players. In 90% of markets, at least one budget player now offers 5G. eSIM availability reaches 92%. Unlimited data, 64%. Streaming bundles, once a premium differentiator, are now available in 40% of markets.

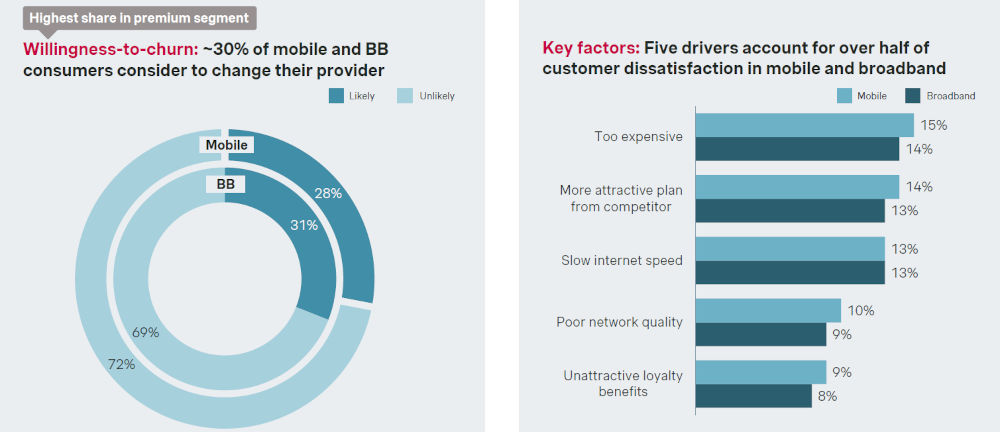

30% are ready to leave – and it's your best customers

Switching intent has crept up incrementally but consistently over the past three years from 28% in 2024 to 30% now. Customers' "fear of missing out" is increasingly triggered by aggressive budget offers. Premium and mid-market customers are most at risk (a 7pp gap vs. budget) as they have more to save and more alternatives to compare.

The main churn drivers point directly back to the value problem: price-value concerns, more attractive competitor offers, slow internet speed, poor network quality, and unattractive loyalty benefits. This shows that churn, along with being a retention issue, is a delayed reaction to weak perceived value and might need some proactive CLTV management.

Source: Simon-Kucher Insights 2026.

The IBRO framework looks at value creation across four areas: Inflow, Base, Renewal, and Outflow – with Brand as the thread connecting them. The simple logic is to build the right brand portfolio, attract the right customers, grow sustainable value in the base to renew the relationship before risk appears, and reduce customer outflow before churn becomes an insurmountable challenge.

Brand portfolio is becoming a structural issue

Brand is an important purchase factor for 70% of premium customers, dropping to 65% in mid-market and 52% in budget – and importance is declining across all tiers as feature commoditize.

That's an argument for sharper brand portfolio architecture. Many incumbents still rely on a single premium brand that leaves the lower end exposed, while budget competition continues to expand.

The average telco operates just 0.8 sub-brands globally. In Europe, where the study estimates 1775 MVNOs, budget-focused competition is particularly intense at 74% compared to just 3% premium. Therefore, as incumbent brand portfolios are least equipped to respond and compete, this is effectively leaving the budget market to MVNOs.

The asset most operators are underusing

On average, a mobile customer stays with their provider for 6.6 years. That makes the existing base one of the most important growth assets telcos have. Yet many operators still manage the customer base too reactively.

The strongest levers are visible but may be underused. Loyalty program participation results in a +20% CLTV, while telco app engagement drives +17% uplift. Loyalty also has a direct ARPU impact of +12% in postpaid markets and +31% in prepaid. Still, 42% of customers are aware of their provider's loyalty program but haven't enrolled and conversion sits at 50%.

Customer service is another underused lever. Customers whose issues are resolved in more than 75% of first calls show average 6.1 years of tenure, compared with 5.7 years for those below that threshold.

The base also cannot be managed as one average customer. The study identifies four globally consistent personas: Effortless Premium User, Digital Maximizer, Online Deal Hunter, and Budget Simplicity Seeker. Each has different value potential, switching behavior, channel preferences, and monetization paths.

What next for telcos

The commercially urgent question to tackle isn't which persona spends most but which personas in your base are undermonetized but reachable. The next phase of telco growth will not come from selling connectivity more aggressively. It's more important to prove value more clearly – across the brand portfolio, across the customer base, and across every point where customers decide whether to stay, spend, or switch.

For more in-depth insights and graphs, contact us directly or download our free report or contact us directly.

The Simon-Kucher Global Telecom Study 2026 study covers 35 countries across six regions and nearly 18,000 consumers. 149 top telcos were assessed, making this one of the most comprehensive views of global telco commercial health available.